Most of us spend our working years accumulating wealth by saving and investing. For most of us, the goal is to have enough in order to maintain our standard of living in retirement. But how do you know if you’ve saved enough? There is no “one-size-fits-all” answer to this question. In reality, many factors go into determining that final number. In this article, we’ll discuss one of the variables that play a role in determining how much you need to save – the 4% withdrawal rule. You’ve probably heard the question or wondered yourself:

How much can I safely withdraw from my nest egg each year, without running out of money?

Table of contents

You may have heard of the 4% Withdrawal Rule. Simply put, the 4% withdrawal rule states that, all things being equal, if you continue to draw down 4% of your retirement nest egg each year, there is a great degree of probability that you won’t run out of money for at least 30 years.

But before exploring whether that rule will work for you, and what impact it might have on your portfolio, let’s talk briefly about how this rule came about.

The History of the 4% Withdrawal Rule

A financial planner named Bill Bengen first advocated the 4% rule over 24 years ago, in 1994. Eager to address anxious clients’ questions about “safe withdrawal rates,” Bengen looked to data from as far back as 1926. He determined that given a portfolio split evenly between stocks and bonds, a 4% withdrawal rate should provide adequate cash flow for a retirement spanning at least 30 years.

The debate of “safe” withdrawal rates continued with the 1998 research paper, called the Trinity Study.[i] With this research, a group of University of Trinity professors added some additional insight into what “safe” meant. This largely confirmed Bengen’s findings.

As recently as 2011, the Trinity academics used an updated data set from 1926 to 2009 to confirm their assessment that anywhere between 4% and 5% withdrawal should be sustainable[ii] for a portfolio comprising of 50% large-cap stocks.

While academic studies confirm the fundamentals of the 4% Withdrawal Rule, real-life sometimes has a way of throwing you a curveball. Before you start planning to take out 4% of your nest egg regularly, ask an investment professional whether 4% works for you.

Related Reading: When it comes to saving for retirement, how much is enough?

Will The 4% Rule Work for Your Portfolio?

The answer is: It depends!

That answer may sound rather vague and unhelpful. It is, however, the most realistic response to this question. The 4% rule will likely apply to most retirement withdrawal scenarios. You do need to be aware of some limitations that govern its application:

- Portfolio risk exposure: Generally speaking, a balanced portfolio with low to medium risk exposure (50:50 or 40:60 stocks/bonds) should be able to withstand an annual 4% withdrawal rate.

- Rate of Return exposure: A portfolio that consistently returns sub-optimal rates of return over a longer period of time, will not be able to sustain a consistent 4% depletion rate.

- Retirement time horizon exposure: If you are looking at early retirement (in your late 40s or early 50s), that gives your portfolio a shorter growth period (as opposed to retiring in your 60s or early 70s). As a result, you’ll likely need to settle for a lower withdrawal rate earlier on during retirement.

- Inflation exposure: You need to think about what inflation will mean to applying a 4% withdrawal rate. The Bank of Canada (BoC) has an inflation target rate of between 1-3%[iii], with inflation currently hovering at the top-end[iv] of that target. If inflation moves any higher (say to 4% plus), simple math tells you that your portfolio will be highly exposed with a 4% withdrawal rate and sub-inflation rates of return!

How some of these variables might impact your withdrawal plans

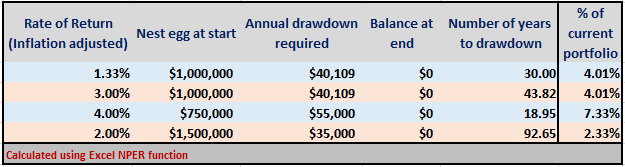

- Based on the hypothetical cases presented above, a $1M portfolio could safely provide you with roughly $40,000 per year for 30 years. Assuming you received a steady inflation-adjusted return of 1.33%. (That’s a 4% withdrawal rate.)

- If that return were to increase to 3%, you could draw down that same amount for much longer – almost 44 years. (Again, if you withdraw 4% from the portfolio each year.)

- However, if you had a smaller portfolio ($750K), and you wanted to withdraw $55k each year, even with a higher return of 4%, your nest egg would only last you about 19 years. (In this case, you’re withdrawing over 7% from your portfolio.)

- And finally, if you start with a larger portfolio ($1.5m), and earn a lower rate of return of 2%, but also withdraw a smaller amount ($35K = 2.3% withdrawal rate), your portfolio could support you financially for 93 years!

Factors that determine what the optimal rate of withdrawal is for each portfolio are the combinations of risk-adjusted, inflation-adjusted portfolio returns, retirement expenditure required, and size of the portfolio.

What’s the likelihood that you’ll run out of money in your retirement?

A Royal Bank of Canada (RBC) study[v] showed that nearly 62% of Canadians surveyed worried about outliving their retirement savings. As a result, the 4% withdrawal rate might be a good start. Just make sure you maintain a disciplined approach to portfolio drawdown. Canadians, however, are living much longer than they did just a few decades ago. Market volatility and inflation are on the rise, so it might be a good idea to have a wealth manager review your portfolio and advise you on your optimal drawdown rate.

Read More: General Tax Avoidance Rule